Authors: Feng Jian, Siqin Bilige, Chen Taotao

From a global perspective, China has consistently been a primary destination for foreign direct investment, demonstrating significant locational advantages. First, China possesses a massive market of 1.4 billion people, with a continuously growing middle-class population and immense consumption potential. Second, its complete industrial and supply chain system provides substantial appeal for manufacturing investment, and China’s manufacturing capacity leads the world. Third, after over four decades of reform and opening up, the quality of China’s labor force has notably improved, with an ample supply of technical talent. Finally, China’s stable development environment and continuously optimized business climate have further strengthened foreign investors' confidence in the country. As a result, foreign investment in China has increased steadily in recent decades, with actual utilized foreign investment rising from 11.01billionin1992to136.32 billion in 2017.

In 2018, despite China’s objections, the Trump administration initiated a trade war, sparking another round of China-U.S. trade disputes. Since then, the narrative of foreign capital withdrawing from China has gained traction. In response to concerns about foreign investors’ confidence, Chinese ministries, including the Ministry of Commerce and the Ministry of Industry and Information Technology, have addressed the issue. For example, in 2019, Miao Wei, then Minister of Industry and Information Technology, responded to journalists, stating that while some foreign capital was withdrawing, other investors continued to increase their investments in China, with overall foreign investment utilization expanding. Similarly, during a routine press conference, the Ministry of Commerce emphasized that China would not retaliate against foreign companies and would strive to maintain the country as the most competitive destination for foreign investment. Despite these reassurances, the debate on this topic remains ongoing.

To clarify the actual situation of foreign investment in China amidst the diverse opinions and better assess the impact of the strategic competition between China and the United States that began in 2018, we extended the timeline to the past two decades. This analysis examines the investment trends of major foreign source countries in China and attempts to evaluate the influence of the trade war.

I. Changes in the Top Ten Economies Investing in China

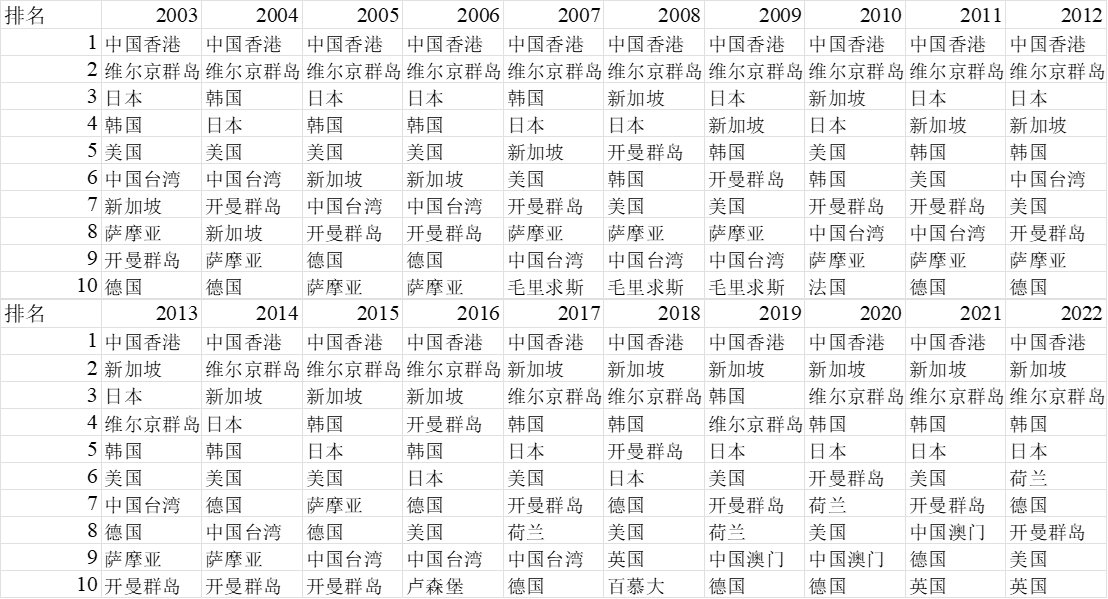

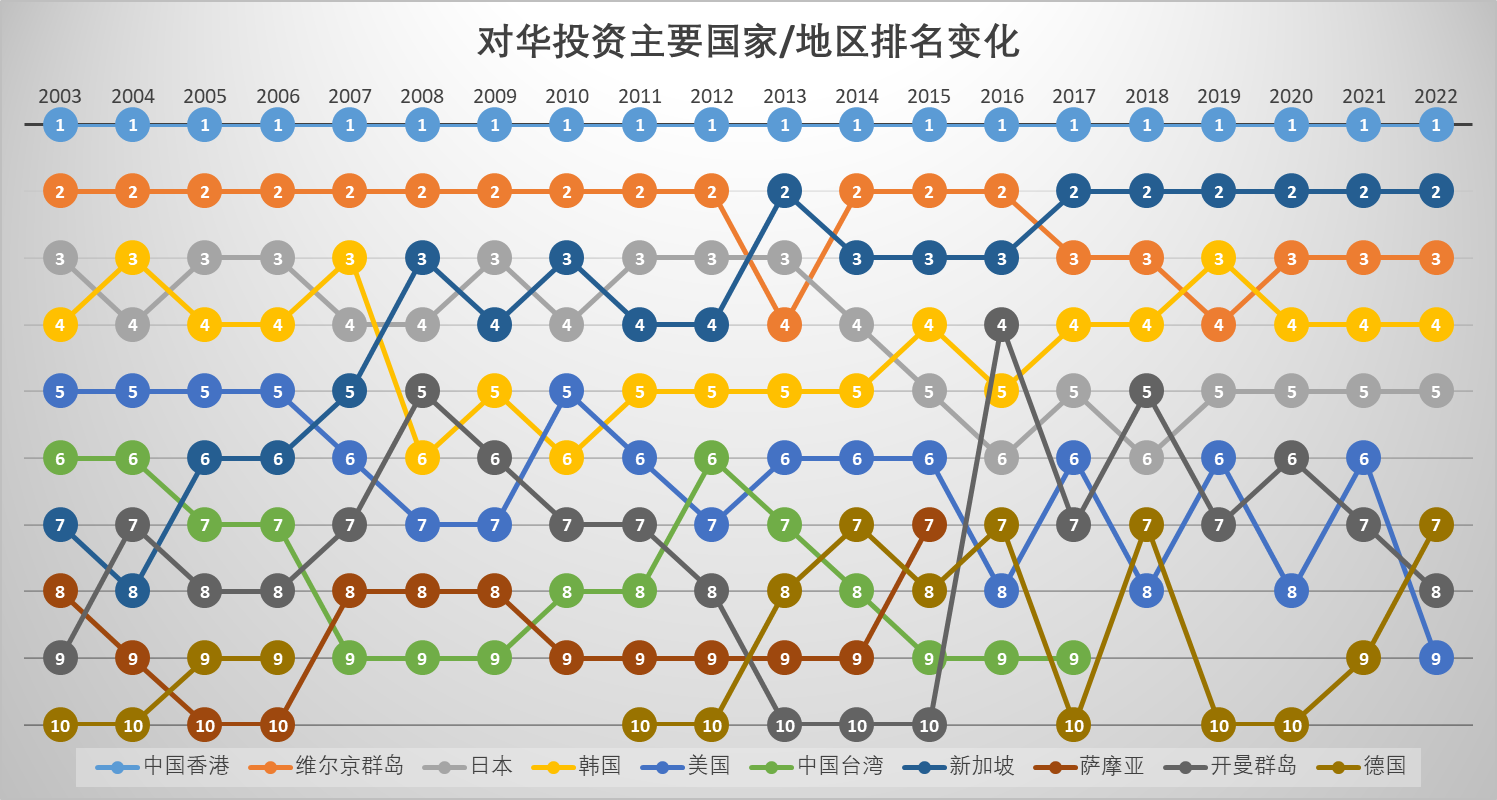

To explore which countries/regions serve as significant sources of FDI for China and whether they have continued to increase their investments, we compiled data on the top ten source economies of China’s inward foreign direct investment (IFDI) over the past two decades. The data sources include the China Foreign Investment Statistical Bulletinand the National Bureau of Statistics, presented in the form of tables and trend charts. Key findings are as follows:

(1) Japan, South Korea, the United States, Singapore, Taiwan (China), and Germany are identifiable primary source economies. Among China’s top ten IFDI sources, Hong Kong (China) holds a unique position, often serving as the "first stop" for foreign capital entering mainland China, making it difficult to distinguish the actual source countries of investments from Hong Kong. Similarly, tax havens such as the British Virgin Islands, the Cayman Islands, Samoa, and Mauritius also obscure the true origins of investments. In contrast, Japan, South Korea, the United States, and other economies are relatively clear source countries.

(2) Around 2016, Samoa and Taiwan (China) began to be replaced by the Netherlands, the United Kingdom, and Macao (China) in the top ten. In the decade before 2016, despite fluctuations in the rankings, the top ten source regions remained largely the same. After 2016, notable changes include: ① Samoa and Taiwan (China), previously in the top ten, fell out in 2016 and 2018, respectively, and have not returned; ② European countries such as the Netherlands and the United Kingdom, as well as Macao (China), began appearing in the top ten, though this has yet to stabilize.

II. Discussion on Key Economies

We separately examine the United States, Japan, South Korea, Germany, and Singapore. The United States is a direct participant in the strategic competition with China. Japan and South Korea are close U.S. allies in Asia and China’s neighbors, with close economic and trade ties. Germany is the economic leader of the European Union, accounting for nearly half of the EU’s investment in China. Singapore is another Asian economy whose investment in China has grown over the past two decades.

(1) United States

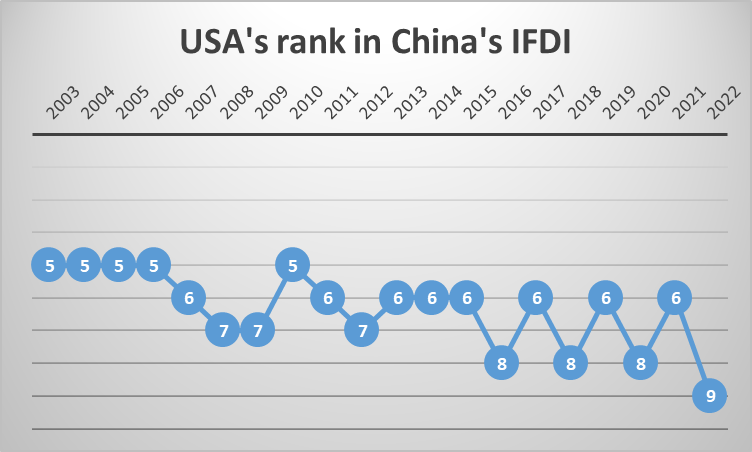

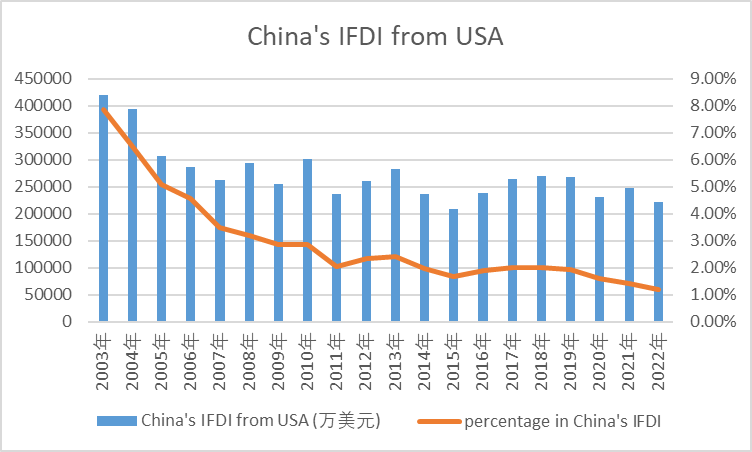

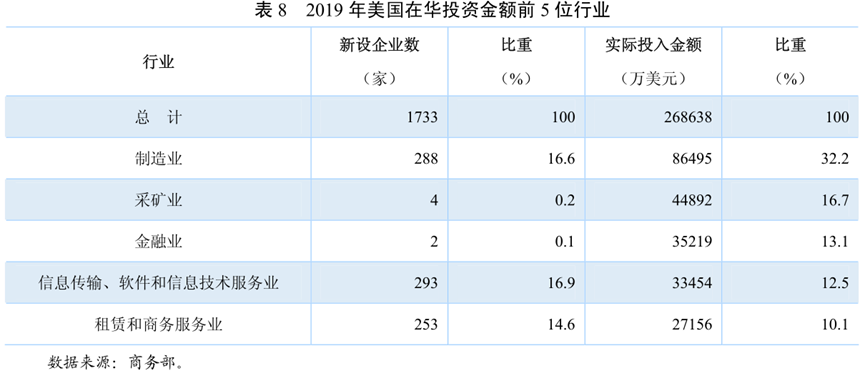

Overall, the United States’ FDI in China has shown a slow decline amid fluctuations over the past two decades. In 2003, U.S. FDI in China totaled 4.20billion,decliningsteadilyto2.21 billion in 2022. The share of U.S. FDI in China’s total IFDI has dropped more noticeably, from 7.85% in 2003 to 1.17% in 2022. By sector, according to the China Foreign Investment Statistical Bulletin 2020, the top five industries for U.S. investment in China in 2019 were manufacturing (32.2%), mining (16.7%), finance (13.1%), information transmission, software, and IT services (12.5%), and leasing and business services (10.1%). These five sectors accounted for 48.5% of newly established enterprises and 84.6% of actual utilized foreign capital.

|

|

The China-U.S. trade friction that began in 2018 has impacted U.S. companies’ investments in China, and the COVID-19 pandemic has also undermined confidence. A 2019 report by the U.S.-China Business Council (USCBC), representing 275 U.S. companies operating in China, showed that 13% of its members planned to relocate production out of China, up 3% from 2018, with increased costs due to China-U.S. tensions cited as the main reason. More tellingly, 17% of U.S. companies decided to halt or reduce new investments in China in 2019, up 9% from 2018, primarily due to increased costs and uncertainty from trade tensions (60%) and the political environment for U.S. companies in China (47%). Recent reports have largely echoed this trend. On August 10, 2023, U.S. President Joe Biden signed an executive order establishing an outbound investment screening mechanism restricting U.S. investments in China’s semiconductor, microelectronics, quantum IT, and AI sectors, which is expected to further impact U.S. investment in China.

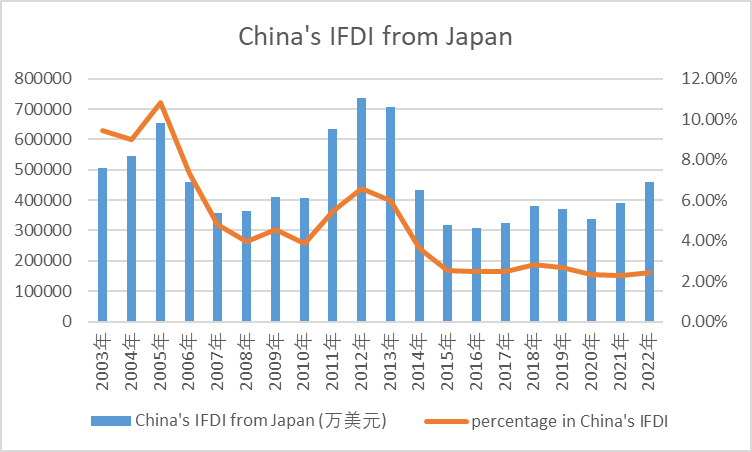

(2) Japan

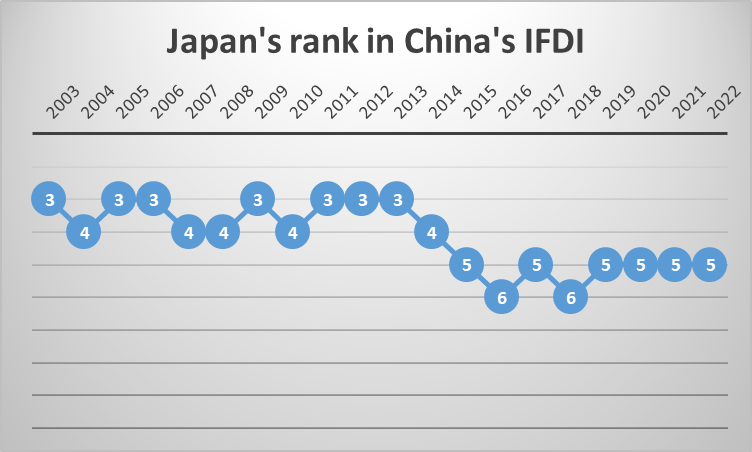

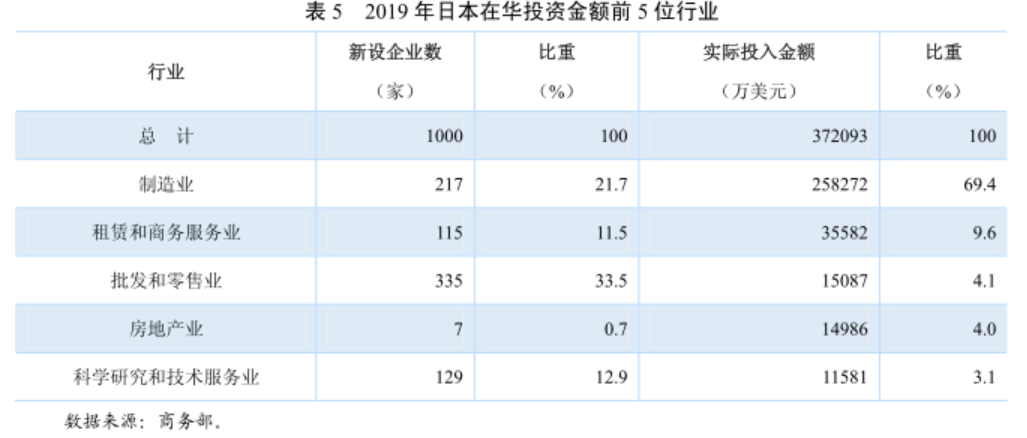

Over the past two decades, Japan’s investment in China has declined from its peak and stabilized in recent years. Before 2014, except for fluctuations around the financial crisis, Japan’s investment in China remained high, consistently ranking third or fourth. However, starting in 2014, Japan’s investment in China dropped sharply and has not rebounded significantly, stabilizing at fifth or sixth place, with its share falling to around 2.50%. Some analysts attribute the 2014 decline partly to uncertainties in Sino-Japanese relations. After the Japanese government announced the "nationalization" of the Diaoyu Islands in autumn 2012, anti-Japanese protests in China led to damage to some Japanese factories and boycotts of Japanese goods, causing some Japanese companies to delay or scale back their expansion in China. By sector, according to the China Foreign Investment Statistical Bulletin 2020, the top five industries for Japanese investment in China in 2019 were manufacturing (69.4%), leasing and business services (9.6%), wholesale and retail (4.1%), real estate (4.0%), and scientific research and technical services (3.1%). These sectors accounted for 80.3% of newly established enterprises and 90.2% of actual utilized foreign capital.

|

|

The China-U.S. trade friction that began in 2018 did not severely disrupt Sino-Japanese industrial chain cooperation. In a 2019 survey by the Japan External Trade Organization (JETRO) of 694 Japanese-invested enterprises in China (with Japanese ownership exceeding 10%), only 5.4% of the companies planned to "downsize" their operations in the next 1–2 years, and 0.9% planned to "relocate or withdraw to a third country/region," totaling 6.3%. Meanwhile, 43.2% planned to "expand," down 5.5 percentage points from the previous year (48.7%), and 50.6% chose to maintain the status quo. Among the reasons cited for downsizing or relocating, only 5% cited "impact of trade restrictions by home or other countries’ governments."

The COVID-19 pandemic likely had a greater impact on Japanese companies in China than the China-U.S. trade friction. In a survey conducted in August–September 2022, 41.9% of Japanese companies in China anticipated a "deterioration" in operating profits for 2022. The main reasons cited included "impact of movement restrictions due to COVID-19" (55.6%) and "rebound decline due to COVID-19" (46.5%).

(3) South Korea

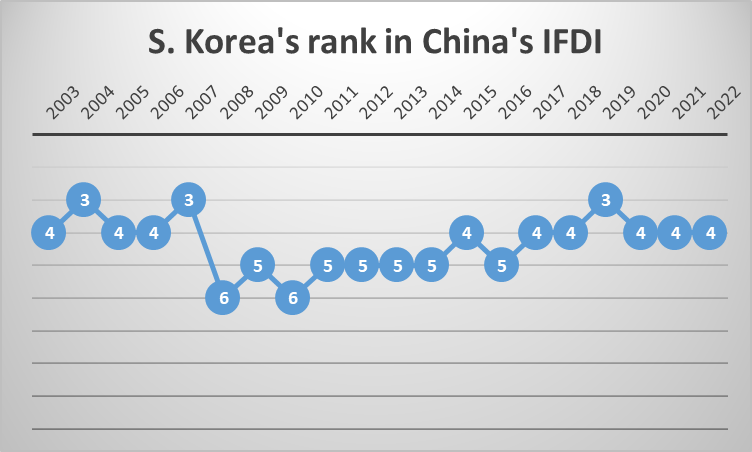

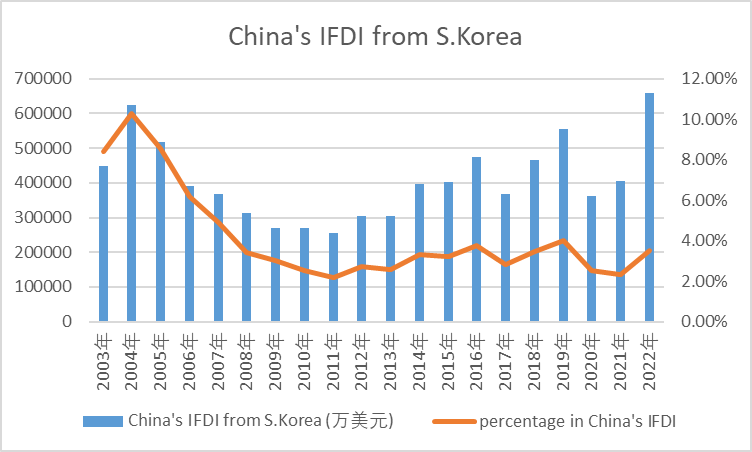

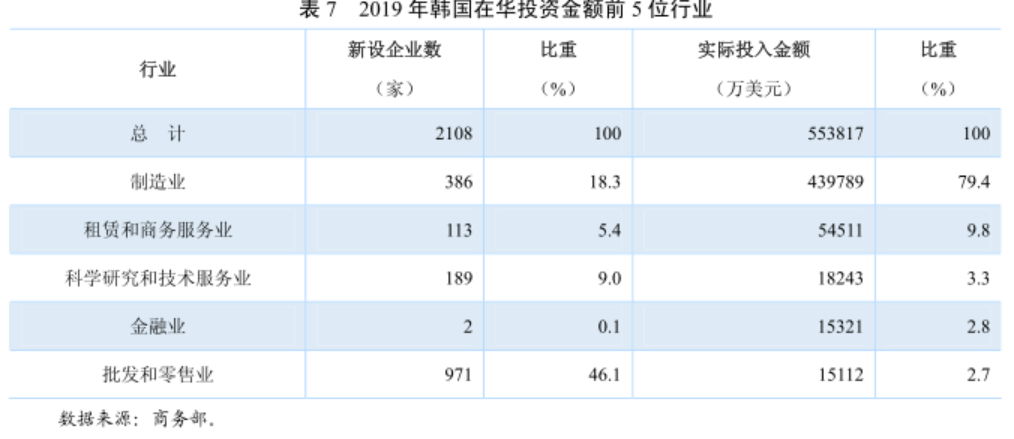

Over the past two decades, South Korea’s investment in China initially declined before fluctuating upward. After peaking in 2004, South Korea’s FDI in China declined year by year, hitting a low in 2011 (2.55billion),withitsshareofChina’sIFDIfallingfrom10.306.60 billion in 2022, surpassing the 2004 peak of $6.25 billion. However, despite the increase in investment, its share of China’s IFDI did not rise significantly, reaching 3.49% in 2022. By sector, according to the China Foreign Investment Statistical Bulletin 2020, the top five industries for South Korean investment in China in 2019 were manufacturing (79.4%), leasing and business services (9.8%), scientific research and technical services (3.3%), finance (2.8%), and wholesale and retail (2.7%). These sectors accounted for 78.8% of newly established enterprises and 98.0% of actual utilized foreign capital.

|

|

The China-U.S. trade friction that began in 2018 did not have the severe impact initially anticipated, though in recent years, South Korean companies have shown a trend toward diversifying and dispersing their overseas investments. South Korea’s investment in China increased from 2017 to 2019 but dropped sharply in 2020, with the pandemic having a greater impact than the trade friction. It rebounded as the pandemic subsided. In May 2022, Sang-Baek Hyun, Director of the China Economic Research Center at the Korea Institute for International Economic Policy, stated at the "Prospects and Development of Foreign Investment in China’s Manufacturing Sector" international forum that contrary to initial expectations, the China-U.S. trade friction had not negatively affected South Korean companies’ investments in China. Currently, South Korean companies’ investments in China focus on high-end manufacturing, particularly semiconductors and components related to new energy vehicles. According to a recent survey of South Korean companies in China, 85.5% noted significant changes in China’s investment environment compared to a decade ago, primarily due to policy risks, intensified China-U.S. competition, stricter environmental regulations, and rising production costs. Notably, South Korean companies now consider both economic and non-economic factors in their investments. Despite some challenges in the current business environment, the willingness of South Korean companies to relocate to third countries or exit China remains very low, at around 3.8%. This is because, after a period of structural adjustment, South Korean companies’ primary goal in China is to tap into the domestic market, whereas previously, they focused more on exporting to third countries. In recent years, influenced by intensified China-U.S. competition and shifts in U.S. foreign investment policies, South Korean companies have expanded investments to regions like North America and ASEAN, showing a trend toward diversification. This indicates that South Korean multinationals are re-evaluating their global production footprint in preparation for global supply chain restructuring.

(4) Germany

Over the past two decades, Germany’s investment in China has fluctuated upward, demonstrating confidence in increasing investments. After the first wave of increased investment from 2003 to 2006, Germany’s FDI in China adjusted downward due to the financial crisis. However, from 2010 to 2018, Germany experienced a second wave of increased investment, peaking in 2018 at $3.67 billion. Subsequently, the pandemic and other factors led to a second adjustment, but recent trends show strong growth again.

(5) Singapore

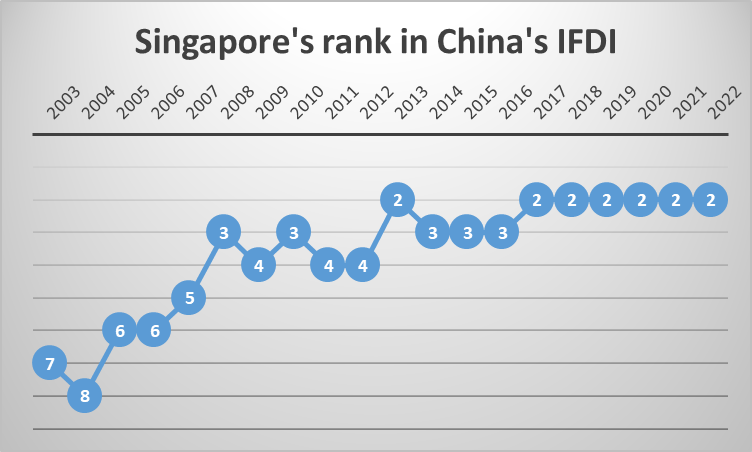

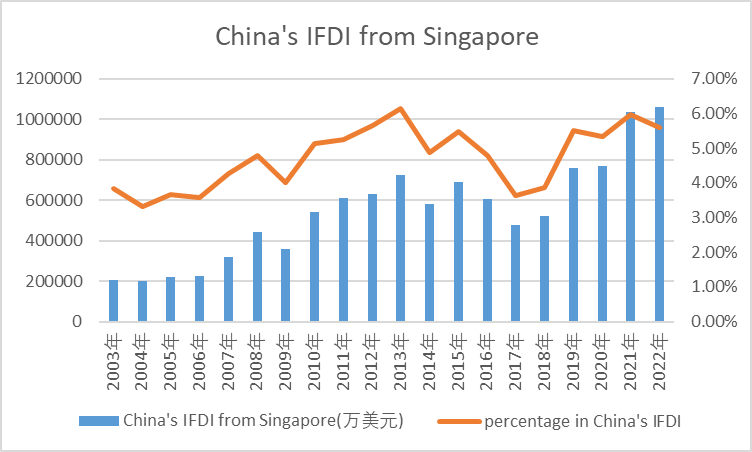

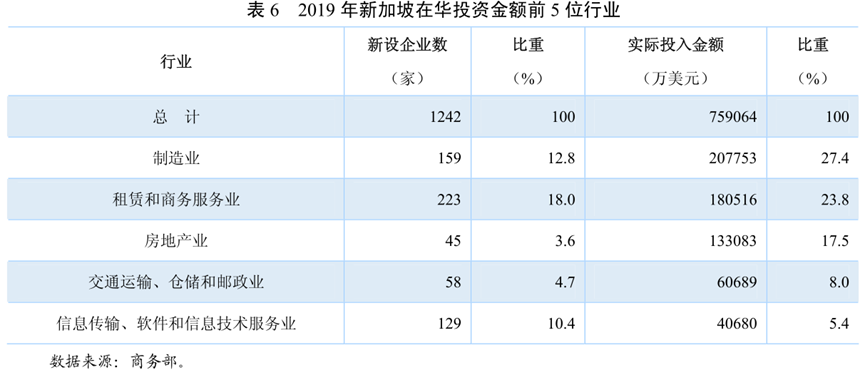

Over the past two decades, Singapore has generally maintained a trend of increasing investment in China, with adjustments only during 2014–2018. Singapore’s ranking among China’s IFDI sources rose from eighth in 2004 to second in 2017, behind only Hong Kong, and has remained there since. Singapore’s investment in China grew from 2.06billionin2003to10.6 billion in 2022, reaching a new high and accounting for 5.60% of China’s IFDI. According to the China Foreign Investment Statistical Bulletin 2020, the top five industries for Singaporean investment in China in 2019 were manufacturing (27.4%), leasing and business services (23.8%), real estate (17.5%), transportation, warehousing, and postal services (8.0%), and information transmission, software, and IT services (5.4%). These sectors accounted for 49.4% of newly established enterprises and 82.0% of actual utilized foreign capital.

|

|

Data suggest that Singapore was not significantly negatively affected by the China-U.S. trade friction. Some analysts argue that Hong Kong’s relatively unstable political situation in recent years and overly strict pandemic control measures threatened its status as the world’s freest economy and hindered international business activities, leading some multinational companies to relocate their regional headquarters from Hong Kong to Singapore. This may have diverted some capital from Hong Kong. However, according to a survey by the American Chamber of Commerce in Hong Kong, only 5% of companies with regional headquarters in Hong Kong were considering relocating. Hong Kong remains the first stop for companies seeking to enter the world’s second-largest economy, and the long-term impact of pandemic control measures appears limited.

III. Conclusion

Overall, the United States, Japan, South Korea, Germany, and Singapore—the major investors in China—share similar concerns about the China-U.S. trade friction, but the extent of the impact varies. After the onset of China-U.S. economic and trade frictions, companies from these countries paid greater attention to potential policy risks, with U.S. companies, as direct participants, most notably affected, as more decided to halt or reduce new investments in China. Although a significant portion of German companies were directly or indirectly affected, their confidence in investing in China remained largely intact. Japan and South Korea maintained close manufacturing supply chain cooperation with China, though in recent years, they have also considered more diversified and dispersed investments to mitigate potential policy risks.

In contrast, in some countries, the impact of the COVID-19 pandemic may have exceeded that of the China-U.S. trade friction. Due to China’s strict pandemic control measures, major manufacturing investors like Japan and South Korea faced significant disruptions, strengthening their tendency to restructure global supply chains and diversify risks.